THERE’S been a substantial surge in slaughter cow prices across Australia, driven by strong demand out of the United States, coupled with attractive margins on cows for Australian processors.

As the table below compiled by Elders analyst Richard Koch shows, saleyards cows for the week ended 10 July (Wednesday last week) averaged 263c/kg across NLRS reported yards, up 26c/kg on the previous week, +46c/kg on a month earlier and 57c higher than this time last year.

The trend is evident in all states bar Western Australia, where advances are still in single digits.

Cow saleyard indicator price for each state against last week, last month and last year. Source: MLA.

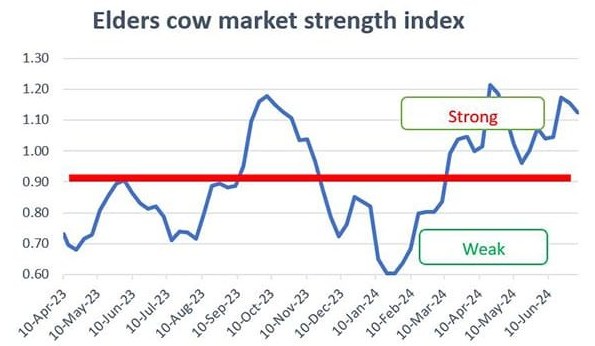

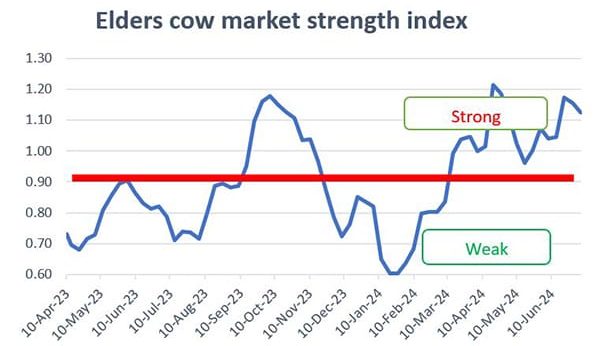

Strong export processing margins on cows have motivated exporters to secure supplies, Mr Koch indicated. This Elders cow market strength index graph plotting processor margins, suggests Australian cow slaughter is currently towards the upper end of the index scale, covering margins over the past 14 months.

Meanwhile in the United States, domestic (US-produced) lean beef prices continue to hold near record levels. Prices last week were approaching US$380/cwt – similar to the record highs seen in the 2014-15 post US drought period, when adjusted for inflation.

Imported lean beef remained firm, but are still trading at a steep discount to fresh domestic US product, the weekly Steiner Imported Beef report said on Friday.

Steiner said the spread between domestic lean beef and imported was currently US70c/lb or more.

“There are more forward offers and more imported product in transit which for now continues to feed the historically wide spread,” Steiner said.

This month’s Australian shipments (to 11 July) to the US have already reached 16,100t, on top of 28,800t for June. Calendar year to date, the US has now taken more than 171,000t of Australian beef, up 75pc on last year.

Will the domestic US to imported lean beef spread narrow, and will this be due to lower domestic lean beef values or higher prices for imported beef?

Steiner’s Friday weekly report said buyers looking to cover their needs in the northern hemisphere autumn (September 1) were well aware of the slowdown in domestic US ground beef demand after the Labor Day holiday weekend (2 Sept) while domestic cow slaughter tends to improve.

“But there are no illusions that domestic prices will come back to where imported values are trading,” Len Steiner said.

“Therefore the key driver for imported prices at the moment is not so much the forward value of domestic prices (be this grinding beef or cuts that could go to the grinder) – rather, the main factor is the potential supply available in the third quarter.”

Overseas suppliers, be this Australia/NZ or South America, had responded to the prices currently being paid in the US.

“The strong US dollar has only added to the impetus to ship product to this market,” Steiner said on Friday.

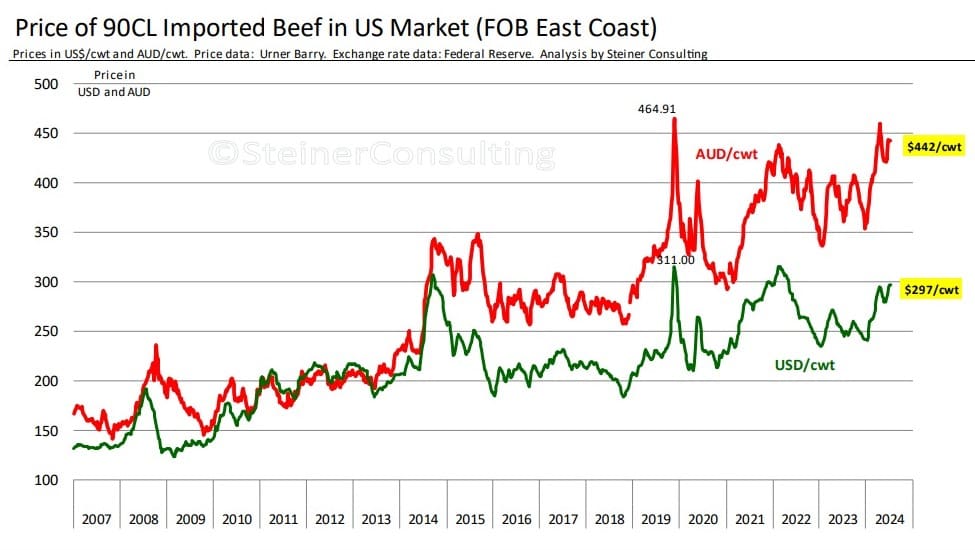

The value of 90CL imported boneless beef (Australia/NZ origin) is currently quoted at around US$297 /100 pounds, up 21pc from a year ago and near the cyclical peak in 2014. However, current prices in A$ terms are about 26pc higher than they were in 2014.

“We are not yet at the levels experienced at the end of 2019, but could potentially get there either later this year or in 2025,” Len Steiner said.

“There has been significantly more product shipped to the US in the last three months, helping bolster imported beef availability and keeping prices from escalating further. Australian beef shipments to the US in May and June were up 57pc, year-on-year.

July shipments, if sustained, project to surpass 40,000t, 74pc higher than a year ago.

Brazil exports still strong, despite tariff

Probably even more surprising has been the surge in shipments to the US from Brazil.

Brazil filled its small ‘other country’ quota to the US back in March, and since then has been lumbered with an additional 26pc tariff.

The out of quota tariff was thought to keep Brazilian exports to the US in check, but that was not the case in June, as shipments were 17,500t, a three-fold increase on last year. New Zealand exports to the US in May were near 25,000t and June shipments are likely to be similar.

Shipments from Argentina and Uruguay are supposed to be limited by quota but that has not been the case so far, Steiner said.

“Argentine beef shipments to the US in May were 4200t, a 200pc increase. We would not be surprised if June shipments were over 4000t again,” Steiner said.

“As for Uruguay, May exports were near 10,000t and up almost 30,000t versus last year for the first five months of the year.

The total US quota available to Uruguay for the year is only 20,000t.

There had been a rush to ship Uruguayan product to the US as buyers looked for alternatives, Steiner said.

“There is also a lot of uncertainty as to how Chinese demand will develop in the second half of the year,” it said.

“For now, however, the big jump in imported beef volume into the US has helped keep imported prices under US $300/cwt, offering exceptional value to both US manufacturers and ultimately US consumers.

“US cow meat supply remains limited. Two short holidays weeks in late May and early July have further contributed to the shortfall just as ground beef demand is in full swing. In the four weeks ending July 13 total US cow and bull slaughter was 427,000 head, down almost 100,000 head (18.6pc) on a year ago, and 30pc lower than two years ago.

Cattle prices start to turn higher

In Australia, Elders analyst Richard Koch said despite a continuation of heavy slaughter (+ 15pc versus 2023 and +12pc on the five year average), prices for slaughter-ready cattle in Australia had started to turn higher in July.

“Export beef prices have risen through the peak demand period (the northern hemisphere summer) and as competition (from the likes of New Zealand) falls in Australia’s major beef export markets.

This, combined with a tightening in supplies of slaughter-ready cattle in the south, has seen southern processors active in northern markets, providing increased processor competition allowing prices to firm, he said.

Strong processing margins lift cow values

Export prices for Australian beef in the US had been on the rise during June, with 90CL lean frozen trimmings reaching A943c/kg last week.

Stronger processing margins have allowed local prices to rise despite continued higher cow slaughter levels, Mr Koch said.

Good signs for heavy export cattle

“While US feedlots remain well supplied with market ready cattle, US fed beef prices have been rising the past month leading into the seasonal peak in US demand around the 4 July Independence Day holiday,” he said.

Normally, US fed beef values started to ease seasonally towards the back end of northern hemisphere summer into autumn as demand for higher value grilling items starts to fall.

“Australia will be looking to demand from North Asian markets to support prices over the next few months,” Mr Koch said.

“Lower competition from US beef in North Asia is assisting Australian beef export values and finished cattle values,” he said.