Click on image for a larger view

JULY has been a hectic month for producers, seedstock breeders and agents with multiple bull sales held across NSW and southern Queensland. To date, just over 50 sales have been conducted, most in NSW, with a strong focus on Hereford and Angus genetics. With sales occurring daily (and in some cases, several on the same day), beef producers may be excused for finding it difficult to keep track of the emerging trends.

Many industry observations suggest that sale results have been variable, rather than reflecting a consistent pattern. This is broadly supported by data from sales held since June. While market confidence has underpinned many purchasing decisions, seasonal conditions have also clearly influenced buyer turnout and competition in different parts of the country.

Persistent drought in southern NSW, Victoria and South Australia has reduced demand from regions that have traditionally supported many sales. In contrast, buyer interest from northern NSW and Queensland has remained steady to strong.

Anecdotal reports from agents and vendors reinforce this shift, with fewer pre-sale inquiries from southern producers and bulls increasingly freighted to areas with more favourable seasonal outlooks. While not universal, this change underlines the role of seasonal confidence in shaping sale outcomes across the country.

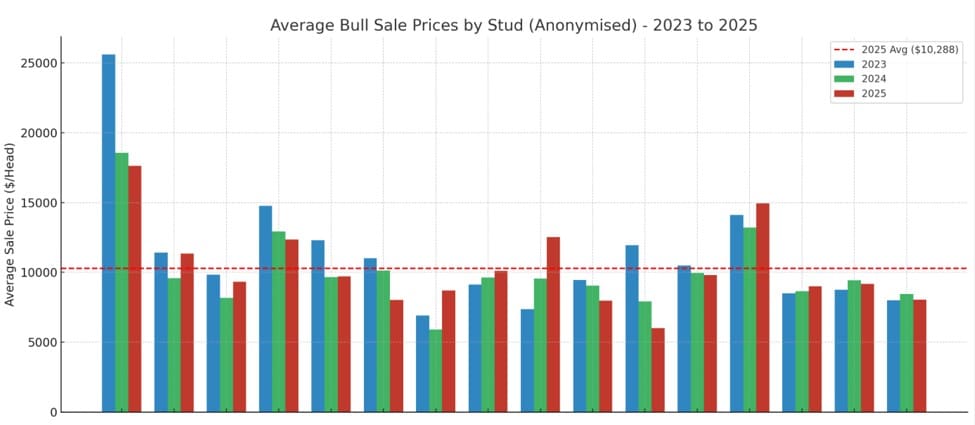

To provide a clearer picture of how this spring compares to recent years, it is useful to focus on those studs that have held sales to date across 2023, 2024 and 2025. The table above reflects the variability in average sale prices that have been recorded in 2025. Several sales have exceeded the industry average of $10,288 per head.

Given the variability that has been recorded from the July sales held so far, it could be difficult for beef producers who are planning on attending sales in August or September to predict what they may have to spend to secure a new sire.

Some broader observations of the sales so far, may help producers in their budget planning ahead of sales.

Most sales held so far have predominately focussed on Angus, Hereford and Charolais bulls. There have been sales that have sold bulls from other breeds, however the numbers represented at this stage of the season are not sufficient to draw any useful comparisons.

In order to be meaningful, only sales that have been held in both 2024 and 2025 have been compared.

Average prices by breed showed divergent trends between 2024 and 2025. Angus increased by 6.5 percent to $12,423 per stud, while Charolais recorded the largest rise, up 24.7pc to $11,413. In contrast, Hereford declined by 9.9pc, averaging $10,383 per stud in 2025.

Clearance rates declined from approximately 93pc in July 2024 to 88.4pc in 2025 for the same group of studs, a fall of 4.6pc. While there have been several high prices this spring, there has been a significant drop in the top prices offered to date.

The mid-market range reflects the prices paid for the middle 50pc of bulls sold, that is those between the 25th and 75th percentiles and is a more accurate indicator of what most buyers are paying. It excludes both the lowest and highest-priced bulls and so avoids distortion from unusually low or high sales.

In contrast, the average price is influenced by all sales and can be pulled upward by a small number of high-value purchases. As a result, the mid-market range is typically lower than the average and offers a clearer view of the broader market activity.

For producers yet to purchase bulls this spring, the key takeaway is to plan with flexibility.

The data confirms that average prices and clearance rates have shifted slightly, and standout prices have been fewer. However, mid-market prices remain relatively stable and are a more realistic guide to budgeting than top prices or breed averages alone.

Buyers should focus on value for money within their preferred genetic profile, rather than chasing price benchmarks that may not reflect broader sale dynamics.

Alastair Rayner

Alastair Rayner is Principal of RaynerAg and an Extension & Engagement Consultant with the Agricultural Business Research Institute (ABRI). He has over 28 years’ experience advising beef producers and graziers across Australia. Alastair can be contacted here or through his website: www.raynerag.com.au