FRIDAY’S United States Cattle on Feed report indicated that cattle numbers in US feedlots were two percent below last year’s level.

On face value, the report would suggest that US beef production is set to decline in an orderly fashion as US cattlemen start to withhold heifers to rebuild herds.

Dig a little deeper and the numbers point to a possible rollercoaster ride in production into the end of the year. Over the summer, US lotfeeders did a good job of withholding cattle from the market to push fed cattle prices and the US beef cut-out (US wholesale fed beef price) to record levels.

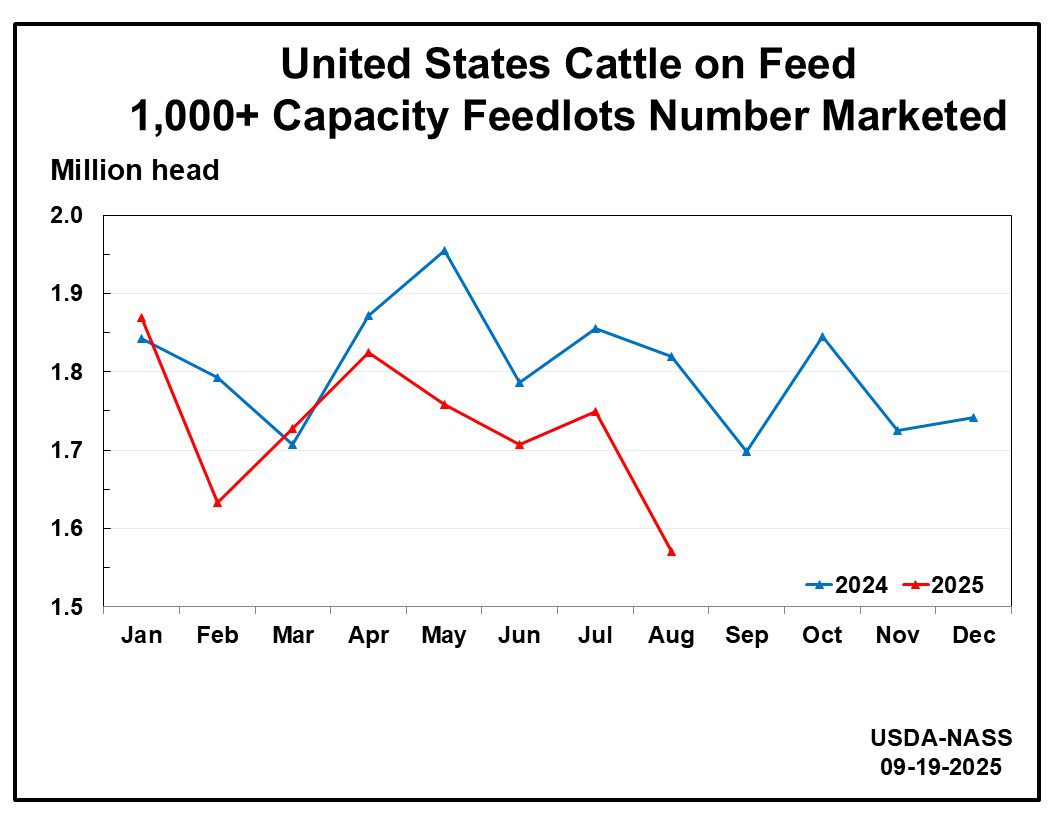

The slowdown in the marketing pace has accelerated since April (marketings of US feedlot cattle in July and in August were down 6pc and 14pc respectively) which has led to a build-up in supply of market-ready cattle in US feedlots.

Marketings of cattle out of feedlots in August were the lowest on record.

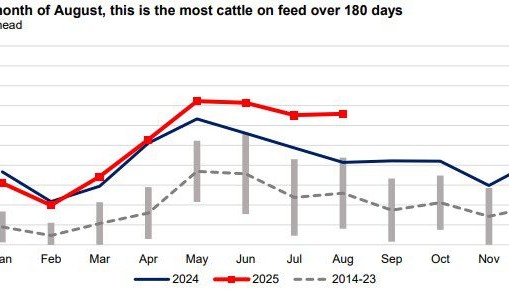

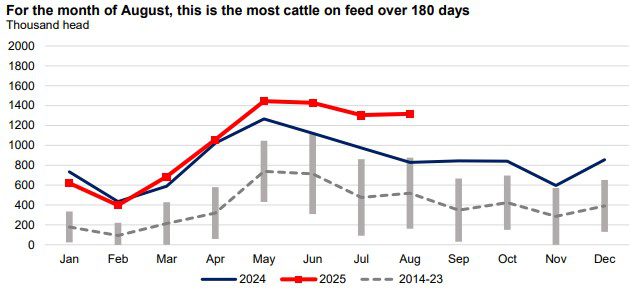

As shown in the chart below, US cattle on feed for +180 days on August 1 were 1.317 million head, or 12pc of total inventories. This is nearly 60pc higher than last year and 8pc more than in August 2020, the previous high for the month. That trend is also reflected in fed cattle carcase weights, rising to a record 878lb (400kg) last week, up from 860lb (390kg) this time last year.

The dip in marketings through August is likely to have further added to the bulge in market-ready cattle numbers in US feedlots.

The USDA Choice grade cut-out is already under pressure, having fallen from a peak of around US$420/hundredweight (CWT) in August to be trading just above US$380/cwt today and will be further under pressure if lotfeeders ramp up marketings over the next few months in a bid to get current.

Strong beef demand

Strong US beef demand and weaker US beef supply have been key drivers of higher beef values over the past year. This may be tested over the next few months if US fed beef turnoff increases, and as the US economy slows potentially leading to lower levels of US consumer spending on beef.

What does it mean for Australia

The impact of lower US fed cattle prices and increased US feedlot turnoff on the Australian beef complex are three-fold:

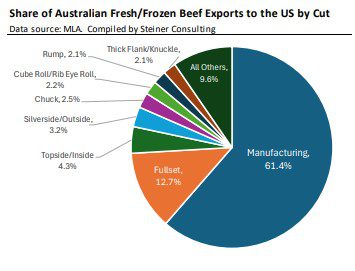

- Firstly, it will put pressure on the value of Australian beef cuts exported to the US. This trade has grown steadily to now represent around 40pc of all beef exported to the US from Australia (see graphic below).

- Secondly, as US wholesale fed beef prices ease, sub-primal beef cuts become available at prices near grinding beef values. For example, USDA Choice outside rounds (flats) were quoted this week at just under $4/lb, about the same as 85CL trim. US domestic 90CL boneless beef was quoted above $4.30/lb. The added availability of these cuts may ease some of the supply pressure on the US domestic lean beef complex.

Thirdly, lower prices for fatty trimmings from higher US fed beef production may support lean imported beef values. US fatty trimmings are mixed with Australian lean beef by US hamburger manufacturers to produce an 80-85pc (lean beef to fat ratio, known as Chemical Lean or CL) beef pattie. So lower fatty trim prices allow manufacturers to pay more for lean beef without affecting the price of a hamburger pattie.

US herd rebuild

But while we are anticipating a lift in US fed beef production as US feedlots offload market-ready cattle into the end of the year, there is light at the end of the tunnel.

US cattle placements have lagged below year-ago levels for most of 2025 as US cattlemen withhold heifers to begin herd rebuilding and due to the US ban on Mexican feeder cattle (screwworm threat).

For the year to July, US feeder cattle imports from Mexico have been a little over 200,000 head versus 850,000 head in the same period in 2024. Eventually, lower placements into US feedlots will lead to a sustained downtrend in US beef production.

To combat the anticipated fall in production toward in early 2026, US feedlots may continue to delay marketings through the back-end of 2025 supporting US fed cattle values and US beef prices.

Much will depend on whether strong US beef demand holds.

As mentioned, US beef demand has been strong through the past summer, enabling record US cattle and beef prices.

US economy slowing

With signs that the US economy is slowing, there may be a pull-back in US consumer spending on beef.

If we see a material fall in US consumer spending on beef, it could lead to a rush of cattle out of feedlots as they seek to limit losses on market-ready cattle.

If US consumer spending holds, they may continue to extend days on feed to plug the hole in fed beef production from falling placements anticipated in late 2025 and the early part of 2026.

Author Richard Koch is Elders’ meat and livestock markets analyst