THE 2025 national bull sale season could be largely described as a stable year. In general average prices per head were up slightly on 2024, and the average top price offered did increase noticeably.

Based on my own records collated throughout the year across 371 auction sales in 12 popular beef breeds (to the end of October, with a handful of Brahman sales still to come), the national average price lifted 4.3 percent to $9854 per head, while the total number of bulls offered rose 4.3 percent to 25,340 head.

Clearance rates held steady at around 85pc nationally, indicating consistent commercial interest despite the contrasting seasonal fortunes between northern and southern parts of the country.

Looking at the broader industry trends as highlighted in the recent Meat & Livestock Australia’s State of the Industry 2025 report, bull sale results have reflected these trends closely.

Higher slaughter volumes, vigorous export demand, as well as signs of herd stabilisation have underpinned producer confidence and willingness to invest in genetics. However the report also confirmed that southern production zones remain under prolonged drought pressure.

Pasture growth has been well below average, feed reserves are depleted, and breeding cow numbers have fallen. The combinations of these factors saw lower autumn bull prices in 2025, and restrained demand for southern bulls during the spring sales.

The seasonal impact has contributed to limited price growth for several British breeds.

By contrast, northern and central regions experienced more favourable seasonal conditions. Producers from northern NSW, Queensland and the Northern Territory continued to invest in sires with proven genetic merit for growth, fertility and in the case of northern programs, adaptability.

This helped drive a measured lift across Bos indicus and composite breeds, demonstrating that commercial demand for high-performing, well-described genetics remains solid wherever seasonal conditions allow.

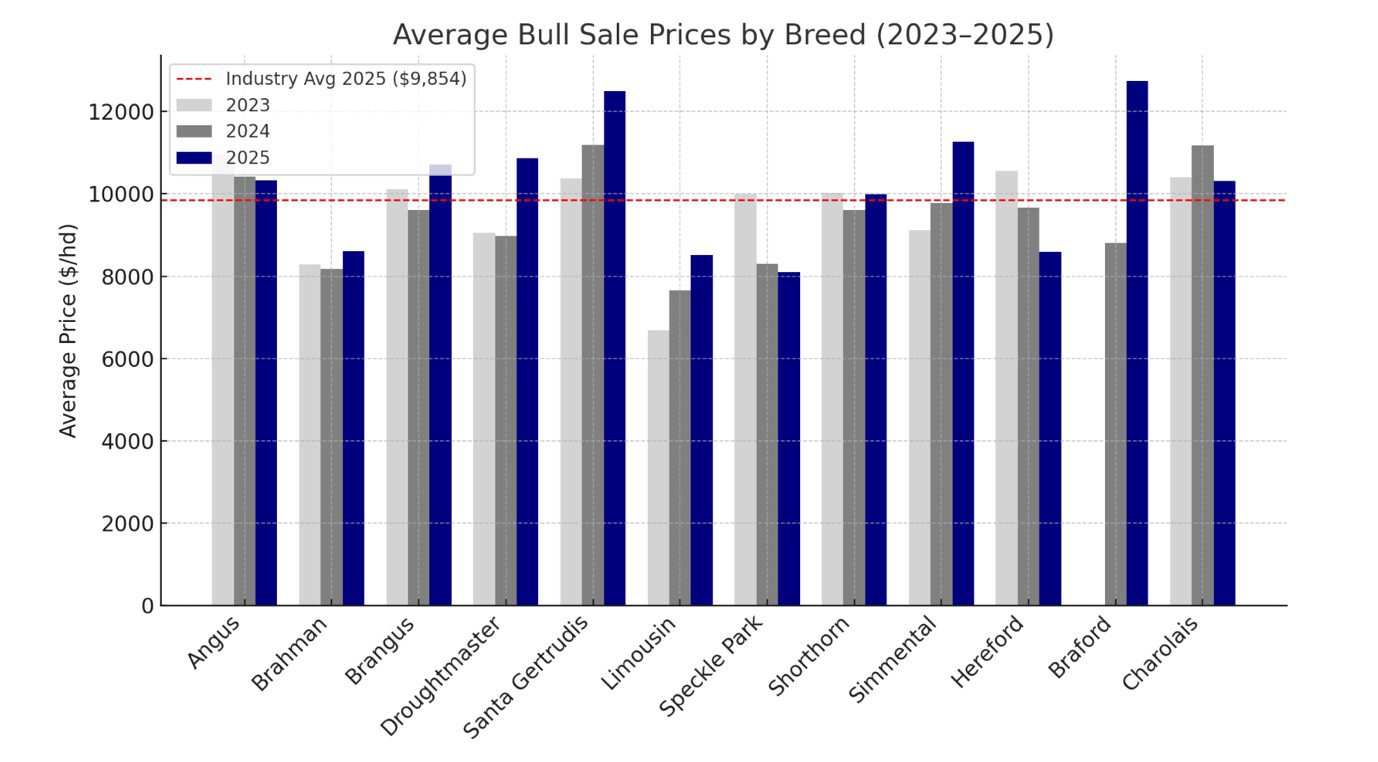

The combined dataset for 2023–2025 shows relatively even price trends for most breeds, though the 2025 year marks a clear divergence as tropical adapted breeds experienced price lifts across most sales.

There was a clear difference, average price wise, between autumn (principally southern) and spring sales across all 12 breeds, with autumn sales averaging $9187 and spring sales, $10,521.

Click on graphs for a larger view

Braford, Droughtmaster, Simmental, and Santa Gertrudis recorded the strongest year-on-year gains, rising by between 10pc and 18pc on 2024 results. These breeds benefited from improved northern seasons and steady commercial demand.

Brangus, Limousin, and Brahman also improved, lifting from 5-12pc. In contrast, the Angus average eased slightly, down 0.8pc to $10,335, while Hereford declined 11pc to $8,599.

These softer southern results largely reflect drought-driven supply constraints rather than reduced demand. A number of established studs in New South Wales and Victoria offered smaller catalogues or postponed sales due to limited feed and reduced breeding cow numbers.

Despite the modest decline, Angus accounted for the largest number of bulls offered in 2025 with around 9300 bulls, or nearly 40pc of national auction sale throughput. Brahman followed with 3970 head, while Brangus and Droughtmaster each exceeded 1500 bulls, reinforcing the continued strength of northern and hybrid programs.

Sale price trends

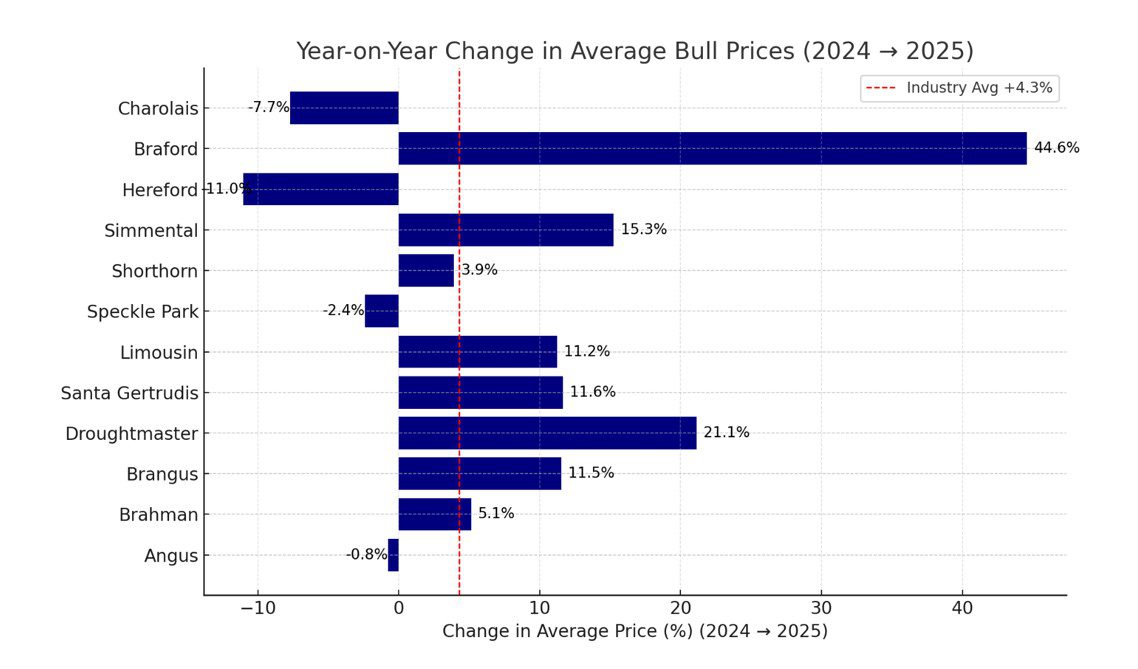

Looking at the change in average sale price from 2024 to 2025 does show several notable changes.

While the industry average (marked by the red line) shows an increase of 4.3pc, the most noticeable gains were experienced by the Droughtmaster, Santa Gertrudis and Simmental breeds, with average prices lifting by between 10pc and 15pc. This was closely followed by Brangus and Brahman with increases of 5-10pc.

These improvements reflect stronger northern seasons as well as confidence in the Bos indicus and composite markets.

Prices for the southern breeds were steadier or slightly lower. Angus eased by less than 1pc, while Hereford, Charolais and Speckle Park fell between 2 and 10pc. These softer results mainly reflect tighter cattle numbers and smaller sale catalogues in drought-affected regions rather than any drop in buyer interest.

Big jump in numbers sold

Based on my records, national sale numbers for the 12 breeds increased from 19,854 bulls in 2024 to 25,340 in 2025.

These increases reflect both new sales added to the national calendar and the resumption of some events that did not proceed in 2024.

Although there were some differences in average prices between British and Tropical breeds, generally overall clearance rates remained firm. The national clearance rate was 85pc, (down 1pc on 2024) which suggests that demand for quality sires remains consistent.

The data also suggests that buyers continue to place value on structured breeding programs and bulls supported by objective performance information.

Across southern Australia, catalogues were smaller in many districts due to reduced breeding cow numbers and feed shortages. Where sales proceeded, buyers were selective, with steady competition for well-presented bulls suited to current feed and stocking conditions.

Commercially grounded recovery

The 2025 sale season demonstrated a measured and commercially grounded recovery in bull sale performance. While overall averages rose moderately, the stability of clearance rates and total volume offered indicate that both seedstock and commercial producers are operating with realistic expectations.

Looking ahead to 2026, the direction of rainfall and feedbase recovery across southern Australia will determine whether the lift in northern breeds broadens into a nationwide rise.

Genetic selection pressure remains strong across all sectors, and the increasing focus on objective data suggests that the Australian seedstock industry is well-positioned to sustain this more balanced, resilient phase of growth.

Final genetics column for 2025

As this marks the final genetics column for Beef Central for 2025, I would like to extend my thanks to Jon Condon and James Nason for the opportunity to contribute to Beef Central throughout the year. I also want to acknowledge the many producers, breed representatives, researchers, and readers who have shared insights, data, and constructive feedback that help shape these discussions. I look forward to continuing the conversation in 2026 as we track the next phase of progress in Australia’s genetic improvement journey.

Alastair Rayner

Alastair Rayner is Principal of RaynerAg and an Extension & Engagement Consultant with the Agricultural Business Research Institute (ABRI). He has over 28 years’ experience advising beef producers and graziers across Australia. Alastair can be contacted here or through his website: www.raynerag.com.au