BUOYED by continued strong northern hemisphere export demand, national cattle slaughter has persisted at high levels late into the 2025 season.

The week ended Friday 5 December shows an NLRS-reported national kill of just over 156,000 head – the sixth largest seven-day throughput for the entire year. That’s close to 6000 head higher than the previous week and more than 12,000 head above this time last year.

All states bar Western Australia showed larger kills last week, with Queensland numbers alone up more than 3000 on the previous week.

All states bar Western Australia showed larger kills last week, with Queensland numbers alone up more than 3000 on the previous week.

Export Manufacturing beef prices have continued to surge as the year has progressed, pushing past A$13/kg (landed US, CIF) in late November, before easing a little last week. Since the start of the year, 90CL beef exports have gradually improved in price, having only rarely exceeded A$10/kg prior to 2025.

It’s been the big driver of slaughter cow prices throughout this year, hitting all-time record highs in recent weeks – surpassing even the 2022 era.

With only eight days’ of operations left at many export plants before Christmas closures start (full list of 2025 plant closure and 2026 opening dates currently being prepared), most export processors have now put the cue in the rack in terms of direct consignment offers on cattle for kills this side of Christmas.

The surge in saleyards offerings in recent weeks (see references below) has probably contributed to that, with many operators filling any remaining late season kill roster gaps with a few cattle out of the yards.

Most large export operators are offering space bookings only for kills in the first week of 2026 operations January. The exception is one large multi-site, multi-state operator which has grids out for week one, 2026, at rates identical to the final grids this year.

We would urge caution in terms of reading too much into that – it’s more about getting a few cattle on the books for re-opening, rather than making any ‘statement’ about 2026 price trends, in our opinion.

Past history suggests it is often closer to Australia Day long weekend before any substantive slaughter cattle price trends start to take shape for the new year.

In southern Queensland, closing active grids for the 2025 year show heavy cows on 750c/kg, and heavy grass steers four-teeth on 830-840c/kg. Both are at, or close to their highest points all year.

Central Queensland plants are 10-20c/kg behind those rates, although the first CQ export sheds have now completed their 2025 season.

In southern Australia, direct consignment grid offers have quality heavy cows still making around 800c/kg and grass four-tooth ox 860c in eastern regions of South Australian and southern NSW.

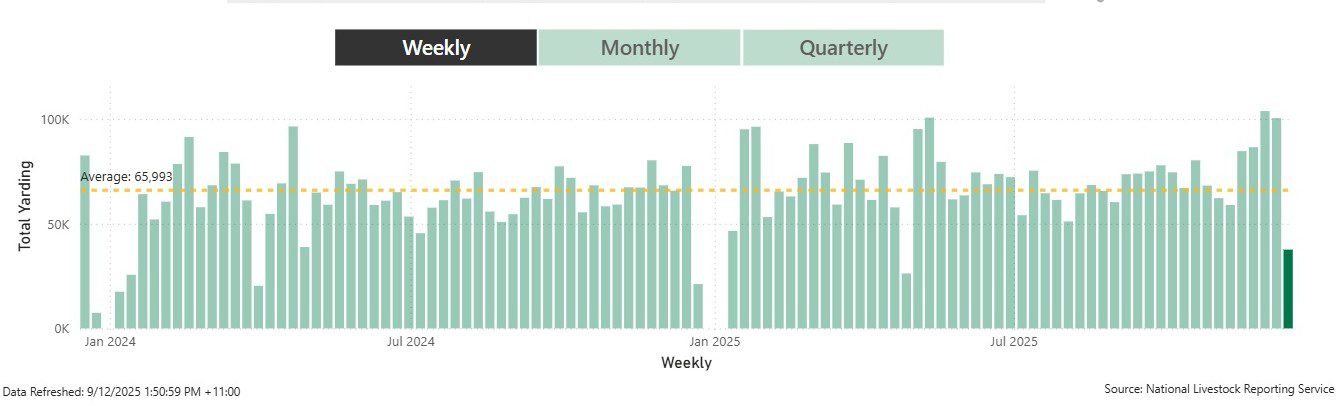

Saleyards numbers surge, but prices falter

The past two or three weeks has seen a substantial surge in saleyards numbers across the eastern states, across both store and slaughter types.

As the accompanying graph shows, the past four weeks has seen the most sustained period of high saleyards turnover all year – well above the two year average of 66,000 head marked with the yellow dotted line. The current, incomplete week at far right, marked in dark green, will expand by the time all sales are completed on Thursday.

Click on image for a larger view

Despite a similar rising cattle market late in 2024, saleyards numbers late last year did not react as they have since late November this year.

We’ll look into the reasons for that in a more comprehensive story tomorrow. Sales held early this week have come under some price pressure, as a result – especially for feeder and slaughter weights.

Saleyards trends

Southern processors have remained active in the Queensland saleyards in early December, providing some price support for cows and heavier steers, but Queensland processors already have most remaining kill slots filled.

Gunnedah yarded 4400 this morning, down 1400 on last week, but still large, by December standards. The quality of the yarding was not to the standard of the previous sale though there were still good numbers of prime cattle in all sections along with good numbers to suit feeders and backgrounders. Young cattle to the trade were up to 20c cheaper with the prime vealers and yearlings selling from 386c to 460c/kg. Feeder steers and heifers were 10c to 15c cheaper with the feeder steers selling from 378-508c/kg. Grown steers and heifers were 6c cheaper with the prime grown steers selling from 390-476c. Cows were firm to 5c cheaper with scores 2 and 3 selling from 318-390c/kg. Prime heavy cows sold from 378-416c to average 397c/kg.

Wodonga yarded 2012 this morning, slightly down on last week. Cows made up almost half the yarding. Demand fluctuated with processors very selective, and feedlots absorbing some of the better types. On the export side heavy steers and bullocks suitable for processors were in reasonable supply, selling within the range of 432-475c/kg. In the cow sale, heavy cows were well supplied however demand softened. The bulk of the heavy cows sold 12c cheaper making from 396c to 432c/kg. Leaner cows D3 types under 520kg were mixed selling from 330-382c/kg.

Roma store sale recorded another unusually large late-season sale this morning, yarding 9455 head – up almost 1500 heads on last week. The overall quality was not up to the standard of the previous week, however the market was firm for lighter restocker type cattle, but softer for heavier feeders and slaughter types Yearling steers 330-400kg sold to 562c to restockers and 524c/kg to lotfeeders. Yearling steers 400-480kg lost ground and made to 514c/kg, while grown steers 500-600kg sold to 424c. Grown steers 600-750kg lost 17c to average 438c.