DRIVEN squarely by vigorous international beef demand, heavy steer and slaughter cow prices have crept to record highs in the past few days – surpassing the blistering market price conditions seen during 2022 when numbers were scarce.

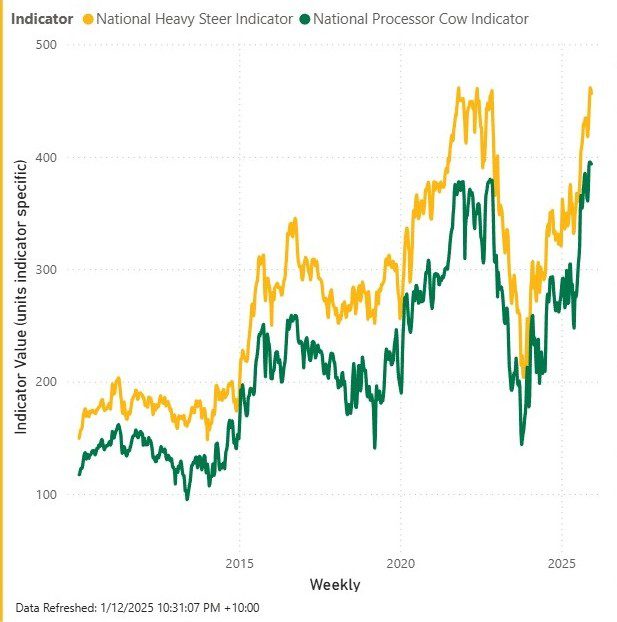

As this graph plotting prices from 2010 to 2025 shows, saleyards processor cows (green) and heavy steers (gold) have both gone past their 2022 record highs over the past couple of weeks. Direct consignment slaughter cattle prices (see summary below) have followed similar trends – now equal to, or even better than 2022-era prices in some regions.

Click on image for a larger view

The circumstances behind current record cattle price highs and those seen in 2022 could hardly be more different.

While export beef demand was reasonably strong in 2022, the big driver that year was herd recovery after the 2019-20 Eastern and southern Australian drought, when slaughter cattle were scarce due to post-drought herd rebuilding and desperate shortage of calves coming through the system.

This year, in contrast, the story is all about demand. The national herd fully recovered to 30.4 million head in 2024, following successive better than average to excellent seasonal years in many areas.

In the September 2025 quarter Australia processed 2.475m head of cattle, the highest quarterly kill in 47 years and slightly above the peak drought-driven turnoff of September 2014. That’s been driven by vibrant demand out of North America and North Asia, particularly, with growth in other markets like the UK, Indonesia and elsewhere.

As the graph shows, saleyards slaughter cow prices have surged since late July, lifting from 328c/kg liveweight on 27 July to 390c/kg today – a lift of 62c/kg or 19pc in four months.

Similarly, heavy steers started their current surge in late July, hitting 463c/kg liveweight four months later in late November (up 100c/kg or 28pc), before easing a little to 450c/kg today. The current easing is partly due to processors getting close to filling their commitments for the 2025 season.

This time last year, Beef Central predicted that 2025 could be a rare ‘goldilocks’ year, where cattle producers, lotfeeders and processors all got a share of the margin. To a large extent, that has proven true, and we’ll dig into that topic in more detail in coming weeks.

Normally, record high cattle prices means processors are left lying bleeding in the gutter. This year, the sheer weight of international demand, unusual market access movements and 70-year herd lows in the US has insulated processors from that, somewhat.

Grid offers steady, as most processors start to focus on 2026

Many processors spoken to for this report are now close to filling their 2025 season slaughter requirements, with just two weeks remaining for many after this week ends, before Christmas closures.

Some are still filling a few gaps with saleyards cattle, but already larger export processors are starting to think about 2026 requirements.

One large multi-site operator has grid offers out for the first killing week next year (weeks commencing 5 or 12 Jan, depending on location) at the current rates listed below.

One large multi-site operator has grid offers out for the first killing week next year (weeks commencing 5 or 12 Jan, depending on location) at the current rates listed below.

We would urge caution in terms of reading too much into that – it’s more about getting a few cattle on the books for re-opening, rather than making any ‘statement’ about 2026 price trends.

Other large multi-state operators are accepting space bookings only for early 2026, content to sit back and negotiate price close to delivery date.

While little business is being done, for what it’s worth, most active grids across Queensland and southern states appear unchanged this week.

Direct consignment offers in southern parts of Queensland this morning still have heavy cows on 750c/kg, and 830-840c/kg on heavy grass steers. The same cows three weeks ago were still making 720-730c/kg.

Central Queensland plants are 10-20c/kg behind those rates, although the first of the CQ export sheds closes its 2025 season on Friday.

There’s still no clear signs of any cattle market reaction to last Friday week’s news that Brazil has gained considerable tariff relief for beef exports into the US, and how that might impact demand for Australian product heading into 2026.

In southern Australia, where good slaughter-weight cattle remain scarce, direct consignment grid offers are also unchanged this week, with quality cows still making around 800c/kg and grass four-tooth ox 860c in eastern regions of South Australian and southern NSW.

- Coming up: 2025 season closure dates and 2026 re-opening dates for major export processors.

Saleyards trends

Numbers lifted by 1250 at Gunnedah this morning, where 5800 were yarded. Cows were back slightly but quality young cattle with preferred heavier weights for the feeders sold well. There was also strong competition for cattle to process and all of the regular buyers were operating in a market that overall sold to a cheaper trend. Grown steers and heifers were 15-30c/kg cheaper with prime grown steers selling from 440-480c/kg and prime grown heifers from 389-440c/kg. Cows were cheaper with score 2 and 3s selling from 272-406c/kg. Prime heavyweight score 4 cows sold from 390-409c/kg.

Roma store sale yarded just short of 8000 this morning, down about 1600 on last week. While cows were yet to sell at the time the interim report was filed, buyers proved selective in their purchases, with some categories losing value. Yearling steers 330-400kg to processors made to 400c/kg, while yearling steers +480kg also to 530/kg. Grown steers 500-600kg sold to 428c/kg and grown steers +600kg sold to to 454c/kg.