A TYPICAL 40-foot shipping container of frozen Australian lean beef trimmings entering the United States market is now, for the first time, worth more than a quarter of a million dollars.

It’s an easy-to-digest metric providing a sign of the times for the supply-starved US beef juggernaut, where demand for red meat remains high, despite record prices for a dwindling pool of domestic cattle, as the national US beef herd hits 70 year lows.

Beef Central has done some ‘back of the envelope’ sums on trimmings prices this week and how they translate into container load value.

Over the past month the 90CL imported cow quote into the US, measured in A$ terms CIF, has passed through $11/kg for the first time in history. It sits tis week at 1110c/kg, having only broken into the +$10/kg range in December. This time last year, the indicator was $1.83c/kg lower than where it sits today, at $9.27/kg, while two years ago, it was worth $2.84/kg less.

Based on this week’s market numbers, a 40-foot reefer container load (max capacity 28t, depending on arrival port) of lean Australian trimmings is worth A$271,000, while even a 20-foot container load (19t) is worth $215,000.

New season buying

Imported trimmings prices have lifted again over the past month or so, as US customers start procurement for 2026.

Purchases being made this week out of Australia means shipping mid-October, and delivery mid to late November, and into the ‘system’ in the US early December, traede sources said this morning.

“But all the big operators in the US are carrying inventory, meaning purchases made this week are unlikely to be used in December, but more likely February or March next year,” one contact said.

“But all the big operators in the US are carrying inventory, meaning purchases made this week are unlikely to be used in December, but more likely February or March next year,” one contact said.

Large stocks of Brazilian beef put aside before the additional 50pc Trump tariff was implemented back in August are now starting to disappear, adding some urgency to recent buying. However it does mean that the full impact of the hefty 76.4pc US tariff on Brazilian beef (Trump’s new 50pc retaliatory tariff on top of the existing 26.4pc since Brazil filled its US quota share back in January) is yet to be seen.

Holding large stocks of frozen Brazilian meat gets expensive. Using the container-load as another example, holding that product in US frozen storage for 12 months adds another $12,500 in interest value alone, before cold storage fees.

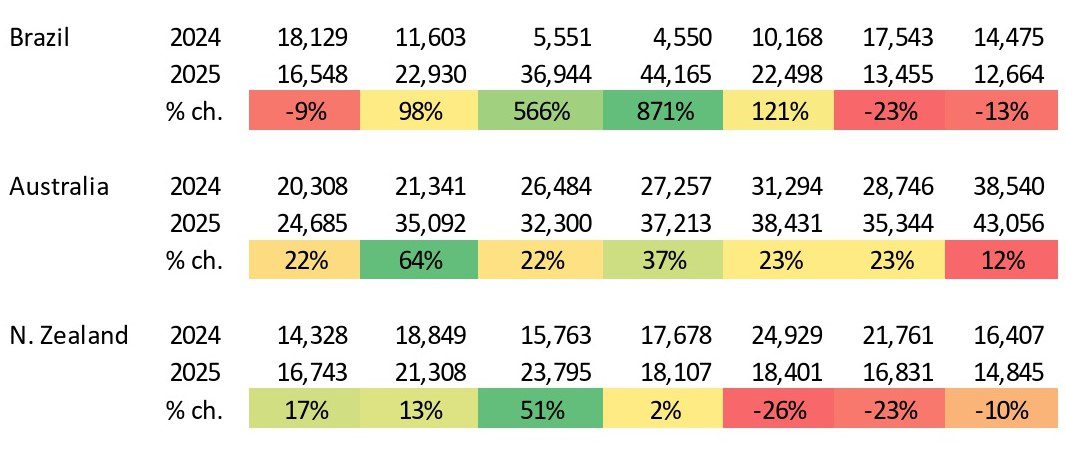

Further to the Brazil tariff impact, August beef export figures from Brazil to the US are yet to be published, but prior months (see table) show Brazilian volumes dropping from 44,000t in April to just 12,600t in July. New Zealand has slipped from its seasonal high of 23,800t in March, to 14,800t in July, while in contrast, Australia has surged 25pc to 43,000t over the same period.

Monthly Brazil, Aus and NZ beef exports to the US – Jan to July 2025

US analyst Steiner Consulting’s latest weekly imported beef market report says US meat buyers returning from Labour Day long weekend found limited offerings and escalating asking prices from exporters.

“We believe a two-tiered market has slowly developed, with large end-users still chasing product given the dearth of offerings from Brazil, and the need to fill production schedules for the rest of the fourth quarter and into early 2026,” Steiner’s report said.

“On the other hand, US processors and distributors that work with smaller end-users are finding it more difficult to reconcile current asking prices, whether for domestic or imported product, with what customers are willing or able to pay.”

“The question that we have come across, be this with market participants or even in social media, is whether current high US beef prices will severely impact demand,” Steiner said.

US beef demand higher, despite elevated prices

In static economic terms, prices did not impact demand, economist Len Steiner said.

“Rather, they simply change the quantity demanded, meaning we move up and down the demand curve. The demand curve shifts, on the other hand, happen because of other factors, such as incomes or consumer preferences.”

Indeed, there had been a significant shift in US beef demand, defined as how much people are willing to pay for a given amount of beef, in recent years.

This year, Q2 demand for beef at retail was 10pc higher than a year ago and 21pc higher than in 2019, Dr Steiner said.

A low unemployment rate, record equity values, a new generation that no longer believes in the ‘low fat’ (anti-beef) dogma, and the insatiable desire to include more protein in the diet have contributed to the shift in demand, he said.

“The biggest risk we see for US beef demand in the next 12 months is a downturn in the economy and the potential for higher unemployment and a foodservice recession. But those that talk about high prices impacting demand are not entirely off-base. A sustained price shock that is not accompanied by a timely adjustment in quantity supplied eventually may affect actual demand.”

“Markets are dynamic, and if prices for ground beef remain high enough, this could cause families to change their eating habits,” Dr Steiner said. “If beef becomes a luxury good, then it will have a different demand structure than if it were a normal, everyday food item.”

For a luxury good, demand increases more when incomes go up, such as people on the higher-end of the income scale choosing steakhouses rather than other restaurants. But luxury goods are also far more income-sensitive, he said.

“Think of fine wine or lobster. When something becomes an indulgence, the baseline level of everyday demand is permanently changed, which represents a shift in demand.”

McDonald’s concerned about becoming ‘unaffordable’

In another recent signal about US beef ‘affordability, burger giant McDonald’s introduced a cheaper menu line in its US business, precisely because it was looking to fight the perception that it was “no longer affordable for families.”

Launched on Monday, McDonald’s announced Extra Value meals (including drink and fries) including a US$8 Big Mac to counter the ‘affordability’ perception among consumers.

“This is the demand risk that beef – especially ground beef – is facing,” Len Steiner said.

“ So the people on social media and elsewhere, have a point – even though for economists incomes and consumer preferences remain the primary determinants of demand.”

Price spread for imported to domestic should narrow

US official beef import data is reported with a significant lag, Steiner said, meaning July imports released only last week did not tell what happened in August or what to expect in September and October.

“Export data from key suppliers of lean grinding beef reflects the impact of tariffs on shipments to the US. The US dollar can either add to, or subtract from, the impact of the tariffs,” he said.

The combined imported beef volume from all supplier countries in the February through April period was more than 100,000t per month, with April close to 120,000t.

“In the last two reported months (June and July), however, the volume has declined significantly, 76,000t in June and 81,000t in July,” Dr Steiner said. “And this was before the tariffs on Brazilian beef went into effect.

Most countries apart from Australia shipped less beef in July than they did a year ago, although it was unlikely that the double digit increase in Australian shipments was sustainable, he said.

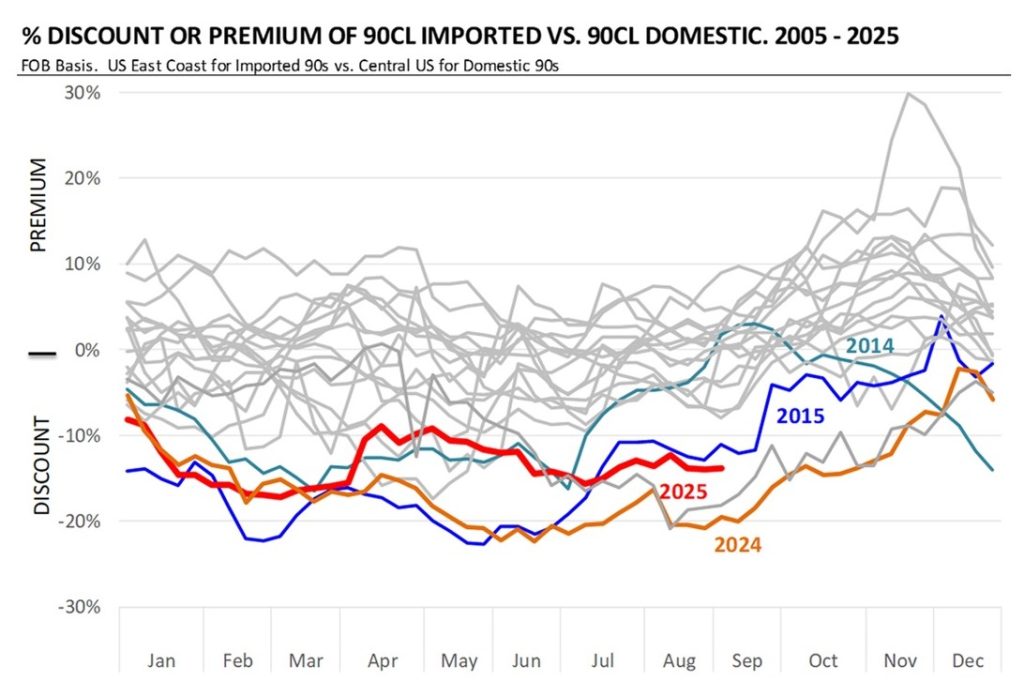

The price spread between domestic fresh lean beef and imports tends to narrow in the northern hemisphere autumn (see chart).

“We think that will be the case again this year, although lack of fresh domestic supply likely means it will once again maintain the premium to imported product,” Dr Steiner said.

Worth noting is the fact that almost all Australian imported trimmings are used in the food service industry (McDonald’s etc), with very little if any imported frozen trimmings finding their way into the other half of the US demand equation – retail sales through Walmart, Krogers and hundreds of other supermarket chains.

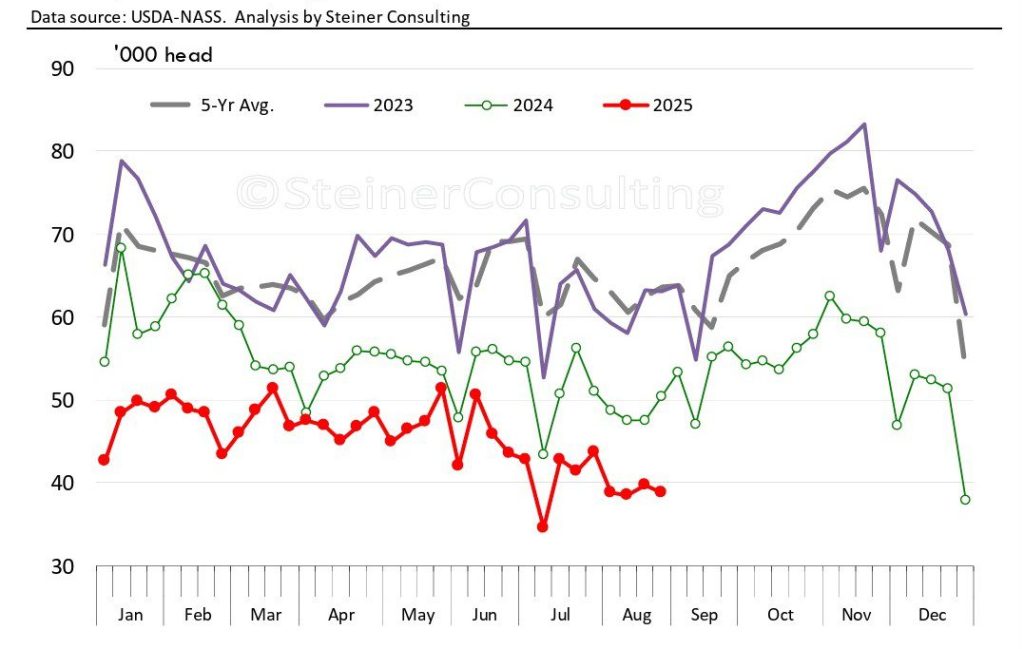

US cow slaughter

Will US cow slaughter recover in the northern hemisphere autumn? Domestic US beef cow slaughter has been particularly limited this summer, Steiner said – a function of improved pasture conditions, a record low beef cow herd, and exceptionally strong profit incentive to hold on to as many cows as possible.

As the graph below shows, weekly US beef cow slaughter in the four weeks ending August 23 averaged 38,900 head per week, 20pc lower than last year and 48pc lower than just three years ago during drought-induced liquidation.

Weekly US beef cow slaughter (000’s)

While US beef cow slaughter may eventually increase by 8000 head from current levels in October and November, it will still be down by double digits compared to last year and previous periods, Steiner suggested.

When dairy cow and beef cow slaughter is combined overall US cow slaughter should be modestly higher than current levels, but still at some of the lowest levels in a decade, Steiner said.