THE saying used to be, “When the US sneezes, Australia catches a cold”, and this has been true for the Australian beef industry for the past five decades as it became increasingly exposed to the global beef market.

By virtue of its size and prominence as both a major exporter and importer, small changes in US beef production can have large consequences for Australian exporters.

By virtue of its size and prominence as both a major exporter and importer, small changes in US beef production can have large consequences for Australian exporters.

Across the span of its cattle cycle, the US can move from being Australia’s largest competitor to being our largest customer.

Currently, the Australian beef industry is benefitting from dramatically lower US beef production after its herd was liquidated due to a severe and prolonged drought in major US beef producing regions.

But while many are focussing on the decline in US beef production, our attention is shifting southward to the rapid emergence of a major low-cost competitor.

This week we take a deep dive into the Brazilian beef industry; its rising production, what’s driving it and in which markets Australia can expect to feel the presence of Brazilian beef.

Brazilian production to determine the direction of global beef prices in 2026

The outlook for global beef prices in the medium term could hinge on the level of Brazilian beef production.

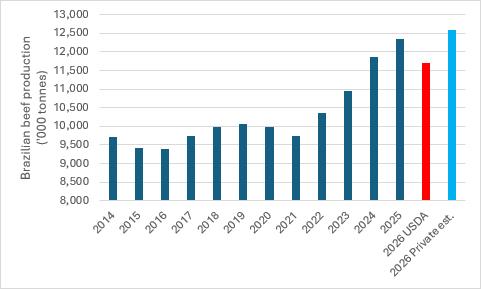

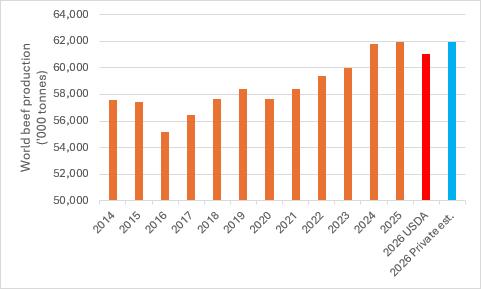

After rising 0.4pc in 2025, the USDA expects output in the world’s six biggest beef producers to fall by a combined 2.4pc in 2026 – the biggest annual drop in decades.

As part of this the USDA is estimating that Brazilian production will fall 5.3pc to 11.7 million tonnes carcase weight equivalent this year.

Source: USDA & private analyst estimates

However, USDA’s estimates diverge markedly from some private analysts that suggest Brazilian beef output could rise (due to productivity gains) again this year, to around 12.6mt in 2026, reducing the decline in production across the top six producers to just 0.2pc.

The divergence in estimates is significant, equating to almost 50pc of Australia’s annual beef export volume.

The Brazilian beef industry has a habit of confounding forecasters.

In 2025 the consensus was that Brazilian beef production would decline by 5pc – when it in fact rose by 4pc. The difference in actual production vs forecasts across an industry the size of is not insignificant, it equates to about the size of Australia’s total annual beef production.

My South American contacts are not suggesting that Brazilian beef production is going to take a step backwards in 2026.

Here is some comment from a market participant in Brazil:

“We are not seeing any production cuts in Brazil – it is quite the opposite. Margins are a bit better compared to the last cycles, and even though there are quotas under discussion, none of the producers are taking that into consideration and local prices are still beneficial for cattle. The Mercosur-EU trade deal recently signed has put a bit more of confidence into the system.”

Source: USDA & private analyst estimates

Click here to view the full article.

The proof will be in whether Brazil can continue to deliver productivity gains, particularly around feedlots. You've got the likes of JBS Brazil on their Q4 earning call at the end of 2025, USDA, and independent analysts all forecasting anywhere between a 3-9% reduction in slaughter numbers next calendar year in Brazil.

With the continued growth in productivity both within Brazilian feedlots and physically at the abattoirs the impact on production volume will be marginally offset, but its difficult to see any growth in production at this time.

Of course, the greater question is, does this even matter when you factor in China beef safeguard quota levels and what this means for where that surplus of export will end up. Even if Brazil do in fact see a minor drop in production volumes this year, I expect North America, Asia, and (to a lesser extent) the EU will all become a buyers market as we move towards the start of the 26-27 FY.

This year, Australia will be looking for a new home for ~90k tns of former China beef exports. Brazil will have ~500k tns looking for a new home too.

The Brazilian Beef Exporters Associations is forecasting exports to the USA of ~400k tns this year, which is 130k tns more than last year.

Something Australian exporters need to plan against is the rapid pace Brazil is achieving in securing enhanced market access across SEA. Brazil just had another 4 abattoirs approved for beef access to Vietnam (8 total now) and 18 more abattoirs are pencilled in for approval for Indonesia in the coming weeks.

Not to mention, Japan isn't immune either, with them out doing listing auditing for a number of new Brazil beef plants in the first half of this year. There are also informal agreements for South Korea and Malaysia to pop out to Brazil to do some this year too.

Most south American analysts I speak to expect Brazilian production to keep rising in 2026. I think the productivity gains they have been making haven't been well understood.

Most analysts missed Brazilian production in a big way in 2025, >500kt. USDA has them pegged at 11.7mt this year but i've heard private estimates of 12.5mt.

The size of Brazilian production could well determine the direction of global beef prices in 2026.....i've never thought that before.

I have been banging on about the threat of Brazil for years. The common pushback was always the same: “They’ll keep getting banned for disease issues.” My response has never changed — “One day they’ll sort all that out.”

That day is fast arising.

Brazil has strengthened its animal‑health systems, expanded market access, and leveraged a feed advantage no major competitor can match. The result is a surge in global influence that is now impossible to ignore.

In 2024, Brazilian beef exports to the U.S. rose 65% — a staggering increase driven by America’s severe cattle shortage and Brazil’s ability to deliver volume, consistency, and price. With the U.S. not expected to recover its herd until 2026–2027, Brazil is perfectly positioned to fill the gap.

China has long been Brazil’s biggest success story. Even with occasional suspensions, Brazil dominates Chinese beef imports thanks to scale, competitive pricing, and improving quality. Australia’s share has slipped as drought, high costs, and limited supply constrain its competitiveness.

As a manufacturer in the Philippines sourcing beef, pork, and chicken, I’ve bought from Australia, Spain, Canada, and Brazil. In the last two years, Brazil has become my primary supplier for all three proteins. They consistently hit specification, deliver reliable quality, and beat competitors on price.

Australia remains a premium supplier, but the competitive landscape has changed. Brazil is no longer the unreliable giant — it’s a disciplined, expanding, increasingly sophisticated export powerhouse.

With the U.S. still short of cattle and China hungry for affordable beef, Brazil is set to grow even further. The warning stands: watch out for the Brazilians — the rise we predicted is now in full swing.

Aye, aye...a serious competitor and Chinese restrictions will accelerate its efforts to gain access to north Asian markets and diversify its beef exports globally.

With cost of living such a huge political issue globally, the time is ripe for lower cost Brazilian product. High-cost beef producers such as the EU & US will be faced with a dilemma, provide access to lower cost beef or continue to protect inefficient industries at a cost to the taxpayer or consumer.