Australian flat iron steak (seamed oyster blade) in a UK steak restaurant

THREE years after the UK-Australia Free Trade Agreement came into force, beef export volumes into the United Kingdom have finally started to show some encouraging signs.

Export volumes were moving at glacial pace for the first couple of years after the FTA agreement was enacted back in May 2023, but recent activity suggests the market is now starting to deliver.

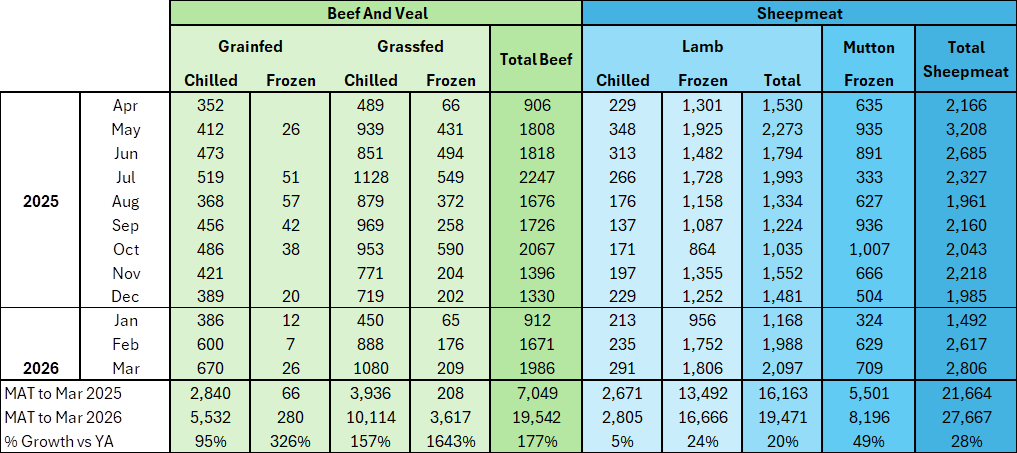

As reported on Monday, Australian exports into the UK in April hit 2700 tonnes, including 2500t chilled. That’s the largest monthly volume seen (at least in recent history) and more than three times higher than April last year.

For the calendar year to the end of April, volume is at almost 7300t, compared with 2800t for the same period last year. Statistics are hard to clearly establish, but these may be the largest monthly and year-to-date beef numbers into the UK since the 1970s era – before the European Union was struck, when the UK was in fact our largest beef export market.

UK production in decline

Underpinning the recent growth in trade has been a long-term, sustained decline in UK domestic beef production over the past 20 years.

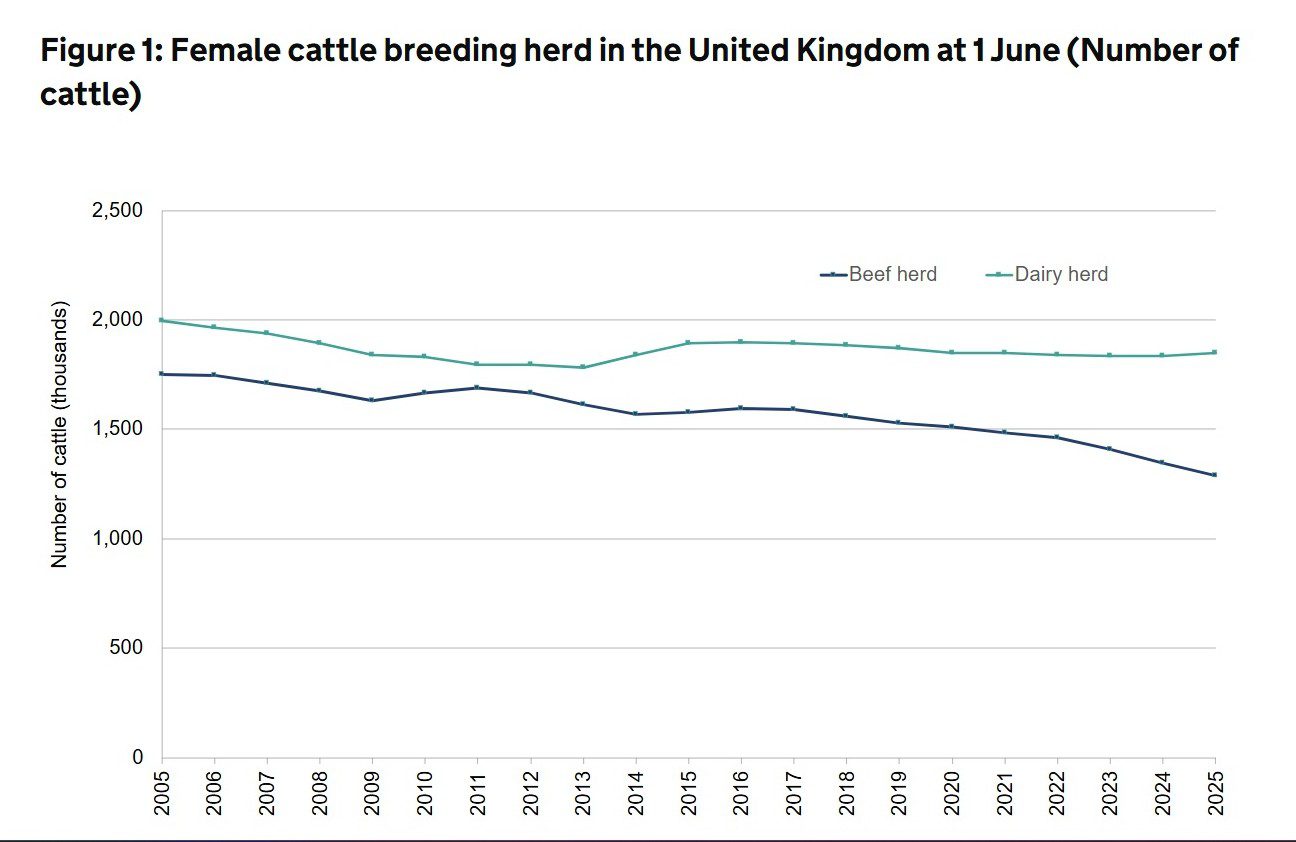

The UK’s Department for Environment, Food & Rural Affairs recently released annual UK cattle population data current to December 2025, showing continued contraction in the UK cattle herd and sheep flock.

Click on image for a larger view

As can be seen in this graph, the long-term trend shows a gradual decline in the UK beef breeding herd, down from around 1.75 million to 1.25 million between 2005 and 2025. Dairy breeding cow numbers over the same period fell from 2m to 1.8m.

The UK sheep flock is moving in the same direction. The national flock totalled 20.45m in December, down another 2.1pc year-on-year. The English (as distinct from the broader UK) sheep flock contracted by 5.5pc to 9.4m.

Clearly, the UK is struggling to maintain earlier levels of self-sufficiency in red meat production, and it is starting to be supported more by complementary – rather than competing – Australian product.

Even at current levels of trade, export volumes are well below quotas that apply under the UK-Australia FTA struck three years ago. Calendar year volume from Australia last year reached 16,865t – roughly one third of our 2025 quota allowance of 51,000t. This year the quota is about 60,000t, but volume is unlikely to reach half that figure.

However the UK could play a role in the back-half of this year in filling the void left after Australia fills its 2026 quota in its other major HGP-free market – China – in coming months.

As Australian product volume into the UK has grown, the product mix has diversified, with grainfed product showing 95pc growth over the 12-month cycle to March, compared with the previous year.

Frozen grassfed (including trimmings for manufacturing meat) has recorded extraordinary growth, lifting to 3600t for the rolling 12 months ended March, up 1600pc on the year before. Some of that goes into applications like beef jerky and biltong, both growing in popularity in the UK under the high-protein diet movement.

It was not coincidental that Australia for the first time mounted a strong MLA-backed display at the UK’s major IFE Hotel, Restaurant and Catering trade show in London last month (click here to view Beef Central’s earlier article).

The range of Australian beef and lamb exporters participating in the event all reported fruitful outcomes from meetings with potential new customers, as well as existing contacts.

Australian exhibitors at the London food trade show last month.

Meat & Livestock Australia’s general manager for international markets, Andrew Cox, said the UK market growth that had been seen this year was stable, partnership-based, and complementary to local UK beef production.

“The market is clearly thirsting for Australian product, and knowledge levels about what we offer has grown. The UK trade can now see where Australian product fits, and it is building a strong foundation for the future,” Mr Cox said.

“To keep the beef category supplied, UK customers can obviously look towards the US, South America or Australia – but we’d argue that Australia is the best placed to fill those gaps in the market – from the perspective of animal welfare, food safety, quality, traceability and other attributes,” he said.

“Our grainfed beef fits well in that story, especially given the current tightness of supply of US grainfed beef as an imported option, and the lack of grainfed domestic beef.”

“Australian grainfed Wagyu briskets, for example, have quickly become popular in the UK, carrying the right marbling.”

Mr Cox said three years after the FTA was struck, some Australian exporters (TFI and JBS for example) had established trade operations and distribution partners in London, while MLA had increased its marketing and product education effort.

Mr Cox said three years after the FTA was struck, some Australian exporters (TFI and JBS for example) had established trade operations and distribution partners in London, while MLA had increased its marketing and product education effort.

“We’re now seeing some of that start to pay off,” he told Beef Central.

“But we are certainly not flooding the market. We have the opportunity at the moment to promote products that might be in tight supply out of the US due to their production challenges.

“We’re introducing Australian Wagyu to UK chefs, for example, to are keen to try something new on their menu. Many have already worked as chefs in other parts of world, becoming familiar with Wagyu and how to use it, and are keen to now feature it in the UK.”

Growth in retail, as well as food service

Mr Cox said the Australian industry always thought there was a good space for Australian beef in the UK market, and the FTA had allowed the industry to now explore that.

While the primary footprint for Australian beef has been in UK food service segment (hotels, restaurants, pubs and clubs), growth in retail was also being seen.

“Retail trade into supermarkets is obviously slower, with most large supermarket chains being integrated with domestic supply. That’s not something we are aggressively trying to counter, but there are opportunities emerging – mostly in the form of specials – but over time, we believe UK consumers will become more comfortable with seeing some Australian beef on supermarket shelves, alongside local product,” he said.

“They are obviously already well-accustomed to seeing Irish beef, which is ‘closer to home’ but also New Zealand lamb, which already has a big footprint in the market.

“So the opportunities are there, and the Australian industry is looking to expand its market presence, in a measured way.”

UK resistance

In a departure from once steadfastly solid British and Irish commitments for beef by the country’s major supermarket retailers, chains like Asda over the past 12 months have started selling Uruguayan beef; Morrisons sells a range of Australian beef steaks; and Sainsbury’s is selling New Zealand beef burgers and other items.

Those moves provoked strong criticism from the UK’s National Farmers Union when they started, which described the trend as ‘deeply concerning’ and ‘outrageous’.

Rival UK supermarkets have also weighed-in, in what became an increasingly polarised, and public, debate. Chains like Waitrose and Co-op last year suggested that such sourcing decisions “undermined the industry’s credibility with the UK farming community, contradicting pledges to source 100pc British at a time when British farming needs our support more than ever before.”

So how does Australian beef measure up to domestic in the UK market on price?

“It depends on the segment,” Andrew Cox said.

“Go into Harrod’s, and you’ll find Australian Fullblood Wagyu at an eye-watering price. But in a more generic segment like (grainfed) knuckles, briskets or blades, our product is very competitive – especially as US product is very short in supply. But equally our frozen grassfed product is also competitive, as an industry.”

Have your say